10thquantum

Suneet

EMC: 20% – 25% upside in 1 year

Trade: Long EMC Current price: 26.75 Expected price: 33 Upside: 23% Time: 1 year

Thesis:

Cheap valuations, EMC on a stand-alone basis (stripping VMware) is significantly mispriced, huge cash pile, share buybacks,market leader, taking market share from competitors, sticky business, focus on innovation, smart acquisitions with power to scale them, strong distribution network,faster growing latest emerging storage offerings, growth in virtualization and hybrid cloud.

Company:

EMC Corporation (EMC) is the world’s largest provider of data storage systems offering products, services and solutions to assist customers with every phase in their IT infrastructure. It helps clients in managing and safely securing large quantities of increasingly complex information. It offers data storage, back up and archive, content and infrastructure management, information security, analytics, virtualization, cloud computing, and other services that enable companies to store, manage, analyze and protect data.

Every organization needs data management and hence EMC’s clients are very diverse ranging from financial institutions, social networking, media, manufacturers, healthcare, internet service providers, telecommunications operators, airlines and transportation companies, educational institutions, public-sector agencies, etc.

The company generates revenues from five segments: two being the major: information storage (69.5% of the revenues as of FY13) and VMware (VMW) virtual infrastructure (22.2% of the revenues as of FY13).

As of 31 December 2013, EMC owned 80% controlling interest in VMware (VMW) and held approximately 97% of the combined voting power of VMware’s outstanding common stock.

Problems analyzed:

1. Public cloud: Public cloud, which is growing at an exponential rate, is a threat to EMC and VMware. In public cloud, data is stored and managed by the cloud application provider. This has advantages (especially to start-ups) as the cloud application user has no initial network infrastructure and maintenance cost, all it needs is the internet connection. Public cloud service providers offer storage and computing to organizations as and when needed and how much they need it, as compared to the traditional way of buying storage and systems from EMC (or NetApp) and essentially paying for extra, unneeded capacity (at least initially) and hence they are seen as a large threat to EMC’s traditional business model. It also allows enterprises to get their applications up and running faster, with improved manageability and less maintenance, and enables IT to more rapidly adjust resources to meet fluctuating and unpredictable business demand. Simply put, public cloud reduces enterprise hardware needs which is a threat to EMC and VMware. Also, some of these public could providers (such as Amazon web services (AWS)) are not using EMC and VMware products and services which takes away the growth aspect. Most cloud customers are startups and small and medium-sized businesses. However, public could providers such as AWS and Google are expected to shift focus to large companies soon, heading right into EMC’s and VMware’s sweet spot, which could be a big threat.

Analyze: EMC’s management very well understands that public cloud is a threat and are taking very aggressive measures to mitigate the revenue loss in information storage segment by launching new emerging storage offerings. Also, to compete on the public cloud front, VMware has recently launched vCloud Hybrid. Hybrid cloud is a system that combines public cloud with a compatible private cloud. The private cloud holds crucial data and applications, while the public cloud offers scale and superior pricing.

Though start-ups and even smaller and medium business IT departments are moving towards subscription based public cloud services to save cost the larger enterprises, especially those that have long established investments in on site infrastructure are not. Main reasons why public cloud hasn’t been able to penetrate in larger organizations are:

- With investments already made and networks set up, public cloud could actually be more expensive for them.

- Security is a big concern for these established companies and hence they are not comfortable with external service offerings.

- Big organizations include applications such as Exchange servers, Windows servers, and Oracle databases. Retrofitting these platforms for a public cloud provider such as AWS is no small task.

To transform and improve business, CIOs have to find efficiencies in their current IT environment. EMC supports the vast majority of enterprise customers contained in these environments (is a market leader) and hence is well positioned to help customers optimize and modernize their current IT needs by transitioning from existing exchange-servers to emerging technologies such as converged infrastructure, software defined data center and private cloud.

Lastly, EMC and VMware have launched Pivotal, which will provide enterprise-class cloud-computing platform and infrastructure and big data for VMware customers.

2. Open source virtualization software’s: Some companies and public cloud service providers are gravitating towards free and open source virtualization such as Citrix’s (CTXS) XenServer and not VMware’s virtualization software.

Analyze: Though Citrix’s (CTXS) XenServer is freely available its market share in the segment is very small and has been declining. Support, service and maintenance are very important for IT departments which VMware is good at. VMware is a leader with 55% share of the virtualization market.

3. Increasing competition and declining market share for VMware: Market share of VMware has been constantly declining over the last few years (declined to 55% in 2013 from 65% in 2008). Comparatively, Microsoft’s share in the market has gone up from around 20% at the end of 2008 to 28% in 2013.

Analyze: Competition has been increasing with companies like Rackspace, Microsoft, Google, Amazon, and others entering the market. Though VMware’s market share has been declining with increased competition, overall server virtualization market is growing and is still expected to grow 18% annually. VMware has grown its revenues by 23% cagr in last 5 years and growth in FY13 was 13%. VMware is still the market leader with 55% market share and its new internal and acquired technologies should further boost revenues and market share.

4. Majority of the revenues come from information storage segment which is a declining business: Information storage segment makes up 70% of revenues and virtualization 23% of revenues. Information storage business is in a secular decline.

Analyze: Overall enterprise information storage market is growing at a very small pace (1% to 2%) in dollar terms. Though the need for data is unstoppable and is growing exponentially, the slow growth has been mainly due to reduced pricing, database appliances that manage more in-memory computing and fast growing adoption of cloud offerings and software-defined storage that reduce enterprise hardware needs. Hardware market has stagnated at current levels as price declines offset most of the growth in unit shipments. That said, EMC is the market leader and has been taking market share from competitors. Its information storage revenue (70% of total revenues) increased by 4.5% in FY13 and its market share in the storage hardware segment increased to 33% in 4Q13, which is double IBM (second in the list) and triple its nearest competitor, NetApp (NTAP). The company is gaining market share because of its strongest and most complete portfolio, aggressive focus on R&D and innovation along with right acquisitions leading to outstanding new emerging technologies and solutions and excellent service. Also, storage software is growing and is expected to achieve a 7% growth in the next two years. EMC is the market leader in both storage hardware and software with a 34.2% and 23.6% share in them respectively.

Catalysts:

1) Sticky business: EMC operates in a very stick business as it has long-term relationships with its customers and the solutions are sold through multi-year enterprise license agreements. Also, it takes a significant amount of time and effort to set up the networks and servers which makes it difficult for existing customers to move.

2) Faster growing latest emerging storage offerings: Though the overall growth in information storage market is stagnant, EMC has been growing its information storage segment revenues (70% of total revenues) by approximately 5%. The growth isbeing driven by smaller, but much faster growing emerging storage offerings. These latest emerging storage solutions like Isilon (network attached storage), Atoms (cloud storage), VPLEX (virtualization and private cloud) and XtremIO (all-flash storage array) are growing exceptionally well: up 54% in FY13 recording a revenue of USD 1.5bn. In less than two months of availability, XtremIO has already taken the market-leading position and combined product sales for Atmos and Isilon more than tripled in FY13. Also, new products such as ViPR, software-defined storage solution, significantly speed up performance. ViPR got off to a very strong start in 4Q. In September 2013, EMC also launched the new VNX Series, which delivers up to four-times the performance of the previous generation. These latest emerging storage offerings have had y-o-y growth of 73% in 4Q13 and 66% in 3Q13. Although this sub-segment (emerging storage) only contributed about 10% of the USD 16bn information storage segment, the momentum and the growth in these emerging storage offering could boost storage business. EMC intends to focus on emerging storage going forward.

3) VMware is growing: EMC owns 80% of VMware (VMW), which has the largest market share in providing virtualization to enable enterprise customers to deploy private clouds. Medium-sized enterprises are still in the early stages of deploying a server virtualization and this market is expected to grow 18% annually. VMware is uniquely positioned as i) it offers solutions which run on industry-standard desktop computers, servers and support a wide range of operating systems, application environments and networking and storage infrastructures and ii) it is 80% owned by EMC and hence has access to the massive EMC clientele and relationships. VMware has been growing its revenues and FCF by 23% and 29% cagr in last 5 years (13% and 32% in FY13), respectively.

Also VMware is attempting to become a cloud management provider, which is a transformation from offering primarily server virtualization solutions. VMware only recently released its vCloud Hybrid Service and made it available in the US in September 2013. It will roll out this service in other regions throughout 2014. The hybrid cloud service has gained tremendous popularity and despite competitive environment the company’s management tools for cloud are selling very well. Also, its vCloud Government Service is expected to be available in 2H14.

Just like EMC, VMware is also focused on innovation. In November 2013, VMware launched desktop as a service (DaaS) offering, with the goal of simplifying the delivery of cloud-hosted desktops, to any device, anywhere. DaaS is a cloud-based desktop service that delivers virtual desktops running on VMware’s vCloud Hybrid Service. It gives customers the ability to blend public cloud desktops and on-premise VMware private cloud desktops. VMware is also adding virtualized GPU (vGPU) by bringing Nvidia GRID technology to its DaaS platform. This gives VMware 30 million potential users: designers, project managers, engineers, and power users. GPU helps delivering a quality interactive visual experience and has been increasingly used even in mainstream Microsoft Office 2013 and rich HTML5 content on internet.

Lastly, VMware acquired AirWatch, the leader in enterprise mobile management and mobile security, providing software tools required by IT organizations to manage, monitor, and secure mobile devices in their enterprise. This helps organizations empowering the mobile workforce.

Apart from growing virtualization market, VMware will be able to pace the delivery of all these services and solution (DaaS, vGPU, AirWatch) through its network of over 11,000 VMware service provider partners further accelerating its top-line growth.

4) Relationship with existing clients: Vast majority of enterprise workload is supported by client-server era, in which EMC is the market leader. With EMC’s massive clientele and long term relationships and VMware’s seamless integration with EMC products, EMC is better equipped to help customers bridge the gap as they transition from the client-server to cloud computing, big data, mobile, and social networking.

5) Integrated with most big enterprise applications and technology alliances: During 2013, EMC continued to deepen the level of integration between its data protection hardware and software products, as well as with enterprise applications from Oracle, SAP and Microsoft and virtual infrastructure from VMware and Microsoft. This integrated approach to delivering solutions helps users address challenges associated with exponential data growth, physical-to-virtual migration and cloud computing initiatives. EMC also engages in numerous alliances with other technology companies for interoperability, seamless integration and hence improved the total customer experience. In 2013, EMC delivered significant technology integration and new solutions for SAP, Cisco, Brocade, Citrix, Microsoft, Oracle and VMware to help accelerate customers’ journey to private, public or hybrid cloud. It also expanded its partner ecosystem with global and regional technology and solutions providers.

6) Strong distribution network and sales force: One of the EMC competitive advantages is its massive direct sales force and distribution network. EMC markets its products and services through direct sales (in North America, Latin America, Europe, the Middle East, South Africa and the Asia Pacific region) and through multiple distribution channels (including value-added resellers and distributors, cloud service providers, systems integrators, outsourcers, independent software vendors, and original equipment manufacturers). EMC and VMware have demonstrated to be market leaders by continuing to dedicate significant resources towards expanding their product scope organically and through acquisition and then maximizing those investments by leveraging their significant distribution capabilities.

7) Focus on innovation with massive R&D expense: The current need for innovation is extremely important as the IT infrastructure market is going through the biggest and most disruptive (and opportunistic) transition. Withinternal annual R&D expense of USD 2.7bn and 15,000 engineers, it is difficult to beat EMC on innovation. Investment in R&D and new technologies and solutions is reflected in numerous innovations, refreshes and successful product launches in 2013. The company continues to develop a product portfolio with customers’ current and future needs in mind.The company continues to make major investments in new business areas including NSX, DCHS Pivotal, ViPR, ScaleIO, XtremIO and Project Nile.

8) Smart acquisitions with strong sales force help reach the product to its massive client base: EMC acquired eleven companies in FY12 and five in FY13. It has a track record of making smart acquisitions and have generated very attractive ROIs on them. Examples include VMware, Data Domain and Isilon. EMC’s strong sales force and partner network help reach the product to its massive client base which creates such attractive returns.

9) Top-line growth faster than it shows: Growth in EMC’s unearned revenues has been much faster than the actual growth in the top-line revenues. Revenue growth was 8.5% and 6.9% as compared to growth in unearned revenues of 22% and 19%, in FY12 and FY13 respectively. This shows the growth has been faster than actually depicted in the revenues.

10) Capex cycle: Cash on companies’ balance sheet is at its all time high but investment in technology has dropped to a near-15-year low as a share of overall investment. Average age of equipment is 7.4 years, the oldest since 1995. Average age of even quickly-depreciating assets like software and information processing equipment is at historical peaks. IT spending could increase significantly with an upturn in the capex cycle.

11) Pivotal: Large volumes of complex data generated by increasing use of smart devices have initiated the need for big data. Smart phones, tablets and new PC form factors are only the beginning. This trend will accelerate as sensors are built into almost every imaginable product that will collectively throw massive amounts of data. The world’s data is expected to expand at a cagr of almost 40% from 2013 to 2020. This data is stored in new clouds quickly and affordably. New and powerful cloud infrastructures provide technology that organizations can use to mine through massive quantities of data and enable them to use their findings to identify new business opportunities, trends and to make better and faster customer-focused decisions by understanding client needs and behavior while improving their operational efficiencies. Pivotal (launched in April 2013 and 84% owned by EMC) is a USD 1bn initiative, offering Platform-as-a-Service (PaaS) to target next-generation cloud and Big Data, as well as agile development tools. It is spun out of VMware, and backed by EMC and GE. The total investments to Pivotal are expected to be USD 400m, most of which will be coming in 2014. Pivotal is predicted to see exceptional growth with potential to exceed revenue of USD 1bn by FY17. A recent IDC forecast shows that the Big Data technology and services market will grow at a 27% cagr to USD 32.4bn through 2017. Pivotal currently contributes just 1.3% of total revenues and could be a huge growth engine for the company in the future.

12) Share buyback and potential shareholder activism: EMC continues to spend more cash on share repurchases. It repurchased USD 3bn, USD 685m and USD 2bn of its common stock from the market in FY13, FY12 and FY11, respectively. In FY12 it also repaid USD 1.7bn of long and short-term debt. In FY13 it issued USD 5.5bn of debt at a weighted average interest rate of 2.4%, taking advantage of the low interest rate environment. Most of this money will be used for stock repurchases and dividend payments. The company expects to spend another USD 2bn on EMC share buybacks in 2014. As per the company, combined payouts of dividends and share repurchases are seen around 50% of free cash flows. With strong annual free cash flow of USD 5.5bn and a massive USD 17.6bn of cash on balance sheet (31% of the market cap) buyback could only increase and the company could be a target for shareholder activism.

13) Valuation:

i) Multiples: EMC is trading at 10x Enterprise Value (EV)/FCF and 8x EV/EBITDA, about lowest historically (even lower than 2009). This is an extremely low valuation for a net debt free technology company, growing its revenues and FCF by 13.6% and 21% on average. In FY13 revenues and FCF grew by 7% and 10%, respectively. The company operates with average FCF margin of 22% and a consistent roce of more than 60%. Assuming a 5 year cagr of 2.8% in top-line and reducing FCF and EBITDA margins by 50bps each year, at current price, EMC trades at a future FY18 multiple of 7.3x EV/FCF and 5.1x EV/EBITDA, as modeled. This also assumes approximately USD 1.6bn (almost 30% of FCF) is used for acquisitions every year. These are extremely low multiple even at a very conservative growth rates. The company expects much higher growth and margins to improve slightly. Twice these multiples (100% appreciation) would be a minimum justification for a market leader in this segment.

ii) DCF: On average EMC’s FCF has been growing by 21% for last 4 years and grew by 10% in FY13. Assuming a conservative growth rate of 3% for next 5 years, a terminal growth rate of 1%, and a discount rate of 10% gives a stock price 20% above its current trading level. This clearly depicts an undervaluation even at minimum growth rates.

iii) Sum of parts:

VMware has had a 5-year average growth of 23%, 26% and 32% in revenues, EBITDA and FCF, respectively. Last year (FY13) revenues grew by 13%, EBITDA by 18% and FCF by 32%. Assuming a 10% growth rate for next 5 years, a terminal growth rate of 1.5%, and a discount rate of 10% gives a stock price trading at approximately current levels.

Standalone EMC: However, EMC on a stand-alone basis (stripping VMware), is trading at extremely cheap multiples (5.4x EV/FCF and 3.6x EV/EBITDA). The core EMC (stand-alone) seems significantly undervalued considering it is a market leader, has been growing its top-line by 5% and taking market share from competitors. Its competitor for stand-alone business NetApp (NTAP), trades at 7.5x EV/FCF and 6.6x EV/EBITDA. Valuing at those multiples suggest an approximate 80% upside on the core EMC (stand-alone) and an approximate 30% upside on the consolidated EMC. Valuing EMC (stand-alone) using a -1% growth rate in FCF for next 5 years, -1% terminal growth rate, and a discount rate of 10% gives a stock price approximately 70% above current trading levels, and a 23% upside on the consolidated EMC. These assumptions are really conservative as revenues from the EMC (stand-alone) grew by 5.2% and 4.5% and EBITDA by 10.1% and 3.7% in FY12 and FY13, respectively.

Even under such conservative assumptions EMC (stand-alone) is significantly undervalued. These valuations remind me of hard disk drive (HDD) manufacturers, WDC and Seagate. In mid 2012 WDC was trading at EV/EBITDA of 3.5x. The rationale behind such low multiples was that HDD manufacturers will not survive as solid state drives (SSDs) are the future. Since then WDC stock has almost tripled. HDDs are still sold and are very much alive.

Conclusion: EMC is trading at a discount even on a very conservative basis and the market is ignoring its competitive advantages including quality, breadth of offerings, strong distribution (sales force and channel partners), after sales service, scalability, interoperability, time-to-market enhancements and expertise in acquiring new emerging technologies with power to scale them. Furthermore its huge cash pile (31% of the market cap), high roce, 10% FCF yield and growing emerging segments are also overlooked. The stock has been down 8% in last 2 years as compared to a 32% gain in S&P on fears of client-server and data storage systems being obsolete with emergence of public cloud. In those 2 years EMC has recorded an average top-line growth of 7.7% and FCF growth of 11.7%.

EMC is taking very aggressive measures to mitigate the revenue loss in information storage segment and so far has been very successful in doing the same. It is well positioned to benefit from the current growth segments of IT: big data, cloud, virtualization, storage, security, and software-defined storage.

Disclosure: Long EMC, NTAP

Disclaimer : This is not an investment advice. DO NOT make any investments based on this article. Please read the disclaimer in detail.

XIV: 30% upside in 3 to 6 months

Trade: Long XIV (short term trade) Current price: 26.6 Expected price: 34.6 Upside: 30% Time horizon: 3 to 6 months

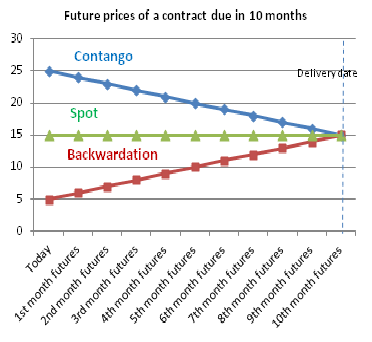

VIX measures 30 days implied volatility of the S&P 500 options. It rises when markets are down and can increase significantly in a day depending on the velocity of the fall. When VIX remains normal to low, we see contango in the VIX futures, which means future prices are above spot price (see figure below). In contango, future prices (which are at a premium to spot price) can be shorted and covered on or before the contract expiration to make a profit (aka roll yield), as future prices decline to converge to spot price as they get closer to expiration date (see figure below).

When VIX spikes, we see backwardation in the VIX futures. In backwardation future prices trade below spot prices (see figure below) and one can play exactly opposite to contango (go long futures and cover the position on or before the contract expiration) to make a profit.

For VIX, there are two important points to consider:

1) Mean-reversion: VIX is the most mean-reverting thing and even in the worst recessions, it hasn’t stayed at elevated levels. It would spike up and then go back to its mean or lower than mean. Below table shows percentage of times VIX has spiked since its inception in 1990 (24 years of historical data), and has remained at those levels.

When VIX level reaches 22 or more, shorting VIX becomes a high probability bet, at least historically. As of 3 February 2014, VIX closed at 21.44. Historically VIX has been at or above those levels only 35% of the times, which means approximately 65% of the times its been below 21.44. Also, at these elevated levels probability of increasing even higher decreases exponentially. For example, as evident in the table above, historically VIX of 22 and above has been recorded only 32% of the times; but 24 and above only 24% of the times. In essence, if VIX spikes up at levels above 22ish, the probability that it will go even higher reduces significantly.

2) Contango: The other advantage of shorting VIX (volatility products) at these high levels is that, historically, VIX futures have been in contango more than 70% of the time and in backwardation less than 30%. As mentioned above, contango is good for shorting VIX futures.

XIV tries to replicate the inverse of the daily performance of VIX. XIV shorts varying amounts of the front and second month VIX futures contracts and covers at expiration. Because of this, XIV collects roll yield, which can be positive or negative depending on whether the VIX term structure is in contango or backwardation, respectively. Since more than 70% of the time VIX is in contango (as mentioned in point 2 above), XIV generates positive yield most of the times. However, since XIV is an inverse ETF and is rebalanced every day, this results in a quite a bit of time decay. XIV has a high volatility, which also means bigger time decay losses.

That said, XIV can be very interesting for short-term trades if you buy it on VIX spikes and sell it in a few months when volatility subsides, due to its mean-reversion nature. As of 3 February 2014, VIX closed at 21.44. As mentioned above, historically VIX has been at or above those levels only 35% of the times, which means approximately 65% of the times its been below 21.44. This means shorting VIX (volatility related products) or going long XIV is a high probability bet. Also, I think the current fall in the market is a correction and VIX should revert back to lower levels. If it does, XIV could see an upside of 30% or more in 3 to 6 months.

Lastly, if you look at chart below, it shows that this is a 3 standard deviation event for XIV, which has never sustained and prices have always risen from such a dramatic decline (mainly due to VIX mean-reversion and that historically VIX futures have been in contango more than 70% of the time).

source: Yahoo finance

Disclosure: Long XIV

Market Timing, key to generating significant alpha

It is very common saying that “market cannot be timed”. Our models below prove that wrong showing a very high probability of timing long-term market tops and bottoms.

We believe in combination of quantitative and fundamental analysis. For timing the market, we try to understand the market as science and constantly experiment by back-testing combination of diverse data-points.

Below models convert our belief in cyclicality, irrational human behavior and market inefficiencies into science by developing 6 proprietary signals (5 contrarian and 1 trend following) indicating long-term market tops and bottoms. When back-tested, one or more of our market timing indicators predicts every fall of more than 15% in S&P since 1965.

Our belief is that market-timing is the key to making big returns and beating the market. Getting one big event right or following one big trend for years and avoiding a downturn can generate significant alpha.

Below are the models:

Interest rates:

This indicator only gives sell signals based on a proprietary formula. It tells when to go on defensive mode and hedge the portfolio from potential losses. The indicator has captured major downturns in S&P such as

1966 (-18% after signal in 8 months),

1969 (-26% after signal in 12 months),

1973 (-39% after signal in 15 months),

1980 (-10% after signal in 1 month),

1981 (-19% after signal in 15 months),

2000 (-46% after signal in 25 months) and

2007 (-45% after signal in 29 months).

It has given 10 signals since 1962, of which most were well-timed and some a little early in the cycle. The indicator is updated on a monthly basis and is a great source to hedge or make an asymmetrical bet. Below is the chart (circled are the ones when the signal did not work).

Speculation:

This is a contrarian indicator which gives buy and sell signals, based on a proprietary formula. It gauges speculation in the market. It gives sell signal when speculation reaches its peak, and vice-versa. The indicator has 100% accuracy when backtested. It gave S&P 500 sell signals in

1972 (-41% after signal in 26 months),

1983 (-7.4% after signal in 10 months),

2000 (-45% after signal in 32 months),

2007 (-51% after signal in 20 months) and

buy signal in

2009 (61% after signal in 25 months).

The indicator is updated on a monthly basis. Below is the chart:

Business cycle:

This is a contrarian indicator which gives buy and sell signals, based on a proprietary formula. It gauges tops and bottoms of a business cycle. The indicator gave S&P 500 buy signals in

1957 (34% after signal in 14 months),

1970 (16% after signal in 13 months),

1974 (42% after signal in 19 months),

1980 (24% after signal in 9 months),

1981 (38% after signal in 20 months),

1990 (36% after signal in 15 months),

2002 (22% after signal in 15 months) and

2008 (22% after signal in 18 months).

It gave S&P 500 sell signals in

1958 (did not work),

1966 (-17% after signal in 8 months),

1972 (-40% after signal in 30 months),

1978 (did not work),

1983 (-8% after signal in 9 months) and

2007 (-51% after signal in 20 months).

The indicator is a great way of making an asymmetrical bet or hedging the portfolio. It is updated on a monthly basis. Below is the chart (circled are the ones when the signal did not work).

Fundamental economy:

This is a contrarian indicator which gives buy and sell signals, based on a proprietary formula. It gives long term bull or bear market indicators. It gauges overheating and irresponsible spending (sell signal) and extreme conservativeness and low points (buy signal) in the economy. The indicator gave S&P 500 buy signals in:

Early 1962: 2% in 12 months but S&P gaining approximately 40% in a continued bull market for next 4 years,

Mid 1993: 1.3% in 12 months but a continued bull market for next 7 years until 2000, with S&P gaining more than 200%,

Early 2009: 35% in 12 months and a continued bull market until now (2013),

Late 2010: 19% in 8 months and a continued bull market until now (2013).

while the sell signals were given in:

2000 (-38% after signal in 23 months) and

2007 (-50% after signal in 19 months).

This indicator is updated on a monthly basis. Below is the chart.

Price growth:

This is a contrarian indicator which gives only sell signals. It gives warning for extreme growth in price. The sell signals were recorded on:

February 1929: -18% after signal in 18 months

November 1936: -44% after signal in 18 months

April 1956: -17% after signal in 19 months

August 1987: -27% after signal in 4 months

July 1998: -14% after signal in 1 month

One wrong signal was given in July 1997 (circled).

The indicator is updated on a monthly basis. Below is the chart.

Trend following:

This is a trend following indicator which gives buy and sell signals, based on a proprietary formula. Basic goal for this signal is to catch the big up-trends in the market and avoid/short significant falls and downturns. It has done a great job by producing a return of 11.7% cagr, as compared to the S&P return of 7.1%, since April 1994 until November 2013 (approximately for last 20 years). Below is the chart:

Apache (APA): undervalued with an enormous optionality on natural gas upside

Trade: Long APA, Short Brent crude

APA Current price: $87

Expected price: $122

Time: 1-2 years

Catalysts: recent strategic acquisitions which have huge potential still to be capitalized, room to improve margins, significantly undervalued to peers, trading below 2008 levels on valuation basis, diversified asset base, enormous optionality on natural gas upside, capex peaking out in 1-2 years, divestures to reduce debt, recently initiated buy-back program, possible shareholder activism.

| Price |

85.04 |

P/tangible book |

1.11 |

Forward P/E |

9.1 |

| Market cap | 33,235 | P/E |

17.26 |

P/Sales |

1.95 |

| EV/EBITDA |

3.73 |

EV/OCF |

5.34 |

EV/FCF |

-44.23 |

| Leverage (Debt/EBITDA) |

1.01 |

P/OCF |

3.91 |

P/FCF |

-32.36 |

Underperformance:

While many oil names just touched their 52-week high, Apache recently touched its 52-week low. The stock reached a peak of 130 in mid 2011 and is currently trading at mid 80s. The fall has been due to significant acquisitions financed via debt and excessive capital spending (capex) on the newly acquired assets, resulting in significantly lower profits, low dividend payments and slower than expected growth. Significant capex outpaced operating cash flow in FY12 resulting in negative free cash flow (FCF). FY12 EPS declined by 56% and recent 1Q13 quarterly EPS declined by 12%. Revenue for the recent quarter (1Q13) declined 10%, on a y-o-y basis.

Additionally, political turmoil in Egypt, where the company generates 20% of its current production, 30% of its current operating cash flow and has 10% of its reserves, is also one of the main reasons for the stock to remain undervalued.

Situation in Egypt:

In February 2011, the former Egyptian president Hosni Mubarak stepped down, and the Egyptian Supreme Council of the Armed Forces took power, announcing that it would remain in power until the presidential and parliamentary elections could be held. In June 2012, Mohamed Morsi of the Muslim Brotherhood’s Freedom and Justice Party was elected as Egypt’s new president. This political turmoil comes with potential threats such as deterioration in the political, economic, and social conditions or changes in laws or regulations in the region, export restrictions, nationalization of APA assets and/or forced renegotiation or modification of existing contracts with the government of Egypt. Management is completely aware of this problem and has met with Egyptian officials, kept production steady, and is actively monitoring the situation. A per management, assets are in very remote areas, and hence the drilling wasn’t affected even while protests engulfed the major cities. The problem is the fear of nationalization of the assets. Losing Egyptian assets would mean a direct 30% hit to APA’s operating cash flow. Apache does mention that as a risk in its recent filing. However, the company continues to receive development lease approvals for drilling in Egypt and plans to invest USD 1.1bn in the region in FY13, highlighting that the situation is not as bad as it seems.

Grown on acquisitions:

The company has grown through acquisitions financing it via debt. The strategy has been to acquire strategic and rich assets at a decent price and then focus on getting value out of them. From 1999 to 2003 APA went on an international acquisition spree to acquire oil rich international assets. From 2009 until present it did the same in the US, focusing on shale plays in the mid-con. During FY10-FY12, APA completed USD 17bn in acquisitions (compared to current book value of USD 30bn), leaving a lot of room for growth in the future. The timing of these acquisitions has been right due to low cost of financing. By acquisitions the company has grown its tangible book value by 11% cagr in last 5 years and 17% cagr in last 10 years. Below is the list of acquisitions:

2012 (Canada): Kitimat, BC, partnership with Chevron: In December 2012, entered an agreement with Chevron to build and operate the Kitimat LNG project. Each will become 50% owner of the proposed Kitimat LNG plant, the Pacific Trail Pipeline, and 644,000 gross undeveloped acres in the Horn River and Liard basins.

2012 (US): Central Anadarko basin acquisition: In April 2012 acquired Cordillera Energy Partners III, LLC (Cordillera), for USD 2.7bn in cash and approximately 6.3 million of APA common stock, increasing the diluted outstanding shares by 4%, from FY12. Cordillera’s properties include approximately 312,000 net acres, basically doubling APA’s position in liquids-rich Anadarko Basin. APA issued USD 5bn fixed-rate long-dated notes in 2012 at an average rate of 3.5% for the acquisition and to pay down maturing debt and commercial paper balances.

2012 (Australia): Yara Pilbara Holdings Pty Limited acquisition: In January 2012, acquired a 49% interest in Yara Pilbara Holdings Pty Limited (YPHPL, formerly Burrup Holdings Limited) for USD 439m. YPHPL is the owner of an ammonia fertilizer plant on the Burrup Peninsula of Western Australia.

2011: North Sea acquisition: In December 2011, acquired Mobil North Sea Limited from Exxon Mobil for USD 1.25bn, adding to other North Sea assets it acquired from BP a decade ago.

2010: Gulf of Mexico Shelf acquisition: In June 2010, acquired oil and gas assets in the Gulf of Mexico shelf from Devon Energy Corporation for USD 1.05bn.

2010 (US): Permian acquisition: In August 2010, acquired acreage and infrastructure in the Permian Basin for USD 2.5bn, net of preferential rights, from BP’s oil and gas operations.

2010 (Canada): Canadian acquisition: In October 2010, acquired BP’s upstream natural gas business in western Alberta and British Columbia for USD 3.25bn.

2010 (Egypt): Egyptian acquisition: In November 2010, acquired BP’s assets in Egypt’s western desert for USD 650m.

2010: Mariner merger: In November 2010, acquired Mariner Energy, Inc. for stock and cash consideration totaling USD 2.7bn. APA also assumed approximately USD 1.7bn of Mariner’s debt with the merger.

Catalysts:

1) Focusing on extracting value from assets acquired: CEO, Steve Farris, mentioned in the 1Q13 earnings call that the company has done enough acquisitions and will now focus on extracting value from them. This would mean high initial capital expenditures on these projects to get them started. APA has an expected capex of USD 10.5bn for FY13. Capex (excluding acquisitions) has increased significantly by 36% in FY10, 44% in FY11, 35% in FY12 and an expected 10% in FY13. Of the USD 10.5bn in FY13, main focus will be onshore North America shale play regions with a dedicated USD 4.6bn capex. USD 2.2bn will be on other projects such as Australian oil developments, Gulf of Mexico deepwater, Wheatstone project, and Kitimat, BC. These significant capex spending would have noteworthy increases in production in the future. Also, with capex peaking in 1-2 years, it would decline in the future boasting free cash flow considerably in years to come. Below are details of the future projects:

i) US shale play: The US contributes 40% of the total production (17% oil, 4% NGL, 18% gas). The Permian, Anadarko and Central Region assets (on-shore U.S. assets related to shale) have huge potential in horizontal drilling with over 88% of the company’s resource potential going forward. That’s where APA has seen the most growth in recent years with liquid production (oil and natural gas liquids (NGLs)) in the US growing by 16%, 28% and 19% in FY10, FY11 and FY12, respectively. In 1Q13, oil production from the US was up 19% and NGLs production 121%, on a y-o-y basis. Natural gas production was only up by 4% as the company is keeping gas production flat due to depressed prices. The US is the strong growth region for the company with its huge recently acquired shale plays. As of 1Q13, about 44% of the current production and 50% of the estimated proved reserves are in the US, a very safe region. In FY13, Apache plans to direct USD 4.6bn of total capex (40%) toward North American onshore regions (mostly in the Central and Permian regions). This focused drilling program should help Apache deliver 25% y-o-y growth in North America onshore liquids (oil and NGL) production.

ii) Kitimat, BC: Canada contributes 16% of the total production (2% oil, 1% NGL, 13% gas) and has 19% of the estimated proved reserves. In Western Canada Apache is working with Chevron on developing the Kitimat LNG project to provide an export route for 50 billion cubic feet of gas reserves in that region. This will increase the total production by 3%. In FY12, Chevron paid Apache USD 400m to buy a 50% stake in Kitimat. The Kitimat plant has received all significant environmental approvals and a 20-year export license from the Canadian federal government. Kitimat is one of the closest ports to the Asian markets, especially Japan, where LNG prices are currently at USD 16 per Mcf, 3x as compared to that in Canada.

iii) Australian oil developments: The company has interests in 30 exploration permits, 17 production licenses, and 13 retention leases that cover a total area of 7.9 million gross acres located in offshore Western Australia. Approximately 90% of this acreage is undeveloped contributing 12% of FY12 estimated proved reserves. Australia contributes 9% of total production (4% oil and 5% natural gas). The production in the region will more than double, increasing by 110% over next 4 years and contributing additional 10% to the total production, with major projects including Macedon (2013), Balnaves (2014), Coniston (2014) and Julimar/Wheatstone (2016) coming online.

iv) Wheatstone LNG: In Australia APA has a 13% piece of Chevron’s giant Wheatstone LNG project, which will come on line in 2016. After coming online, the production is expected to be 11 million barrels of oil equivalent (4% of current total production) annually for 20 years. LNG rates in Australia are at USD 8/MCF, more than double that in the US. APA will be the biggest domestic gas supplier in Western Australia by FY13. APA’s Australian subsidiaries have been already signing long-term sales and purchase agreements for supplying LNG to Asian companies.

v) Forties Alpha: The start of the Forties Alpha satellite platform should add to Apache’s production growth in 2013 (3%-5%) and more than offset the natural field declines continuing in Australia, Canada and Argentina.

vi) Egypt: Egypt is a cash-cow for the company as it generates USD 2.7bn operating cash flow of which USD 1.1bn is spent on capex, with remaining USD 1.6bn in free cash flow, that is used for other parts of the business. The region provides 20% of total production (13% oil and 8% gas). Average sale price of oil in the region is one of the highest at USD 111 per bbl. APA announced three new discoveries in the Western Desert of Egypt during 1Q13, extending the company’s production. The region has 10% of FY12 estimated proved reserves. Even with all the turmoil, the company have continued to receive development lease approvals for drilling in Egypt and plans to invest USD 1.1bn in the region in FY13.

vii) North Sea: North Sea provides 9% of total production (8% oil, 1% gas). The region has one of the highest average sale price for oil (108 per bbl) and natural gas (8.95 per Mcf). APA increased its portfolio in the region by acquiring Mobil North Sea Limited in FY11, which provided the region with additional exploration and development opportunities across numerous fields. This resulted in a y-o-y production increase of 37% in FY12 in the region. The region has 6% of total estimated proved reserves.

2) Reduction in executive pays due to underperformance: Due to significant underperformance of the stock among its peer group, the board has reduced the compensation of CEO, Steve Farris, who is also the chairman, by 18% as compared to previous year and bonus to 150% of the base salary from 200%, as per SEC filings. The shareholders did not pass an advisory vote on compensation of executive officers during the annual meeting on 16 May 2013. Also, the total director compensation was being reduced to USD 300k from USD 350k, with a cut in the equity component of the pay package. Overall, this puts pressure on the management for better performance. I think, the board and the CEO are fully aware that activist shareholders can take greater positions anytime and shake things up if the management does a sloppy job with good assets and doesn’t create value. We have recently seen a lot of shareholder activism in oil and gas sector such as Hess, Transocean and Chesapeake.

3) Divestures, reduction of debt and share buybacks: On 9 May 2013, APA reported 1Q13 earnings and announced a plan to divest USD 4bn in assets by year-end 2013. The company recently hired Goldman Sachs to unload shallow water Gulf of Mexico assets. Another likely divestiture could be Argentinean assets. Fortunately oil prices have remained high, so the company should get good value. APA intends to use USD 2bn to reduce debt and another USD 2bn to repurchase stock under a 30 million share repurchase program. With a current market cap of USD 30bn, this is approximately 7% share buy-back program and puts some floor on the stock price, in case of a fall. Divesting potentially heavy future investment non-core assets, reducing debt and buying back stock would create more value.

4) Recent hedge fund and Insider buying: In 1Q13, quite a few hedge funds were buyers of the stock including T Boone Pickens, Wallace Weitz, Brain Rogers, Third Avenue Management, NWQ Managers, Manning and Napier Advisors, Inc. Diamond Hill Capital, Richard Pzena, George Soros, Louis Bacon, Charles Brandes, Jeff Auxier, Paul Tudor Jones, Jeremy Granthan and Ray Dalio. In Feb, March and April 2013, we saw some insider buying as well.

5) Margins and cost efficiency: APA has lower margins than its peers but that’s where it has the opportunity to improve. OCF margin has declined from an average of 55% in last 6 years to 50% in FY12, due to significant declines in natural gas prices. Also, acquisitions had deviated management focus. However, the acquisition spree has ended and APA is now focusing on costs by reducing drilling days and frac cost by self sourcing and optimizing frac design. With shareholders ousting executives and revamping boards because of poor performance, the pressure to improve margins and be cost efficient is real.

6) Natural gas play with diversified asset base: The company is a less-levered play for the potential upside in the natural gas, due to its diversified asset base both within the U.S. and internationally. If gas prices soar, Apache’s top quality on-shore assets could significantly increase profitability. As of FY12, 45% of APA’s production was oil and 49% natural gas. That said, 78% of revenues come from oil and only 19% from natural gas. This is due to drastic declines in natural gas prices, which has forced APA to focus on liquids where margins are higher and keep natural gas production flat. APA can boost its production with an increase in natural gas prices which could have a significant upside on its revenues and bottom-line. Also, APA took heavy write-offs on its various natural gas assets last year due to lower prices. Increase in natural gas prices would also increases the value of those assets on balance sheet, growing the book-value. Below points highlight the potential increase in natural gas prices.

i) Natural gas prices have declined by 70% in last 5 years, to USD 3.9 mmbtu in June 2013 from USD 13.2 mmbtu in June 2008. This has created a huge divergence between price of oil and natural gas. The chart below shows price of natural gas (per barrel of oil equivalent) as a percentage of oil price. On average in FY12, natural gas was 24% of oil price in the US for one barrel of oil equivalent. This means it could be bought at a 76% discount to oil. This energy source will be exploited in the future and price differential will not remain at these levels.

ii) Many power plants are opting for the cleaner burning natural gas to replace coal and some of that transition is permanent.

iii) Major manufacturers of chemicals, steel, etc are increasing their utilization of, or shifting to, cheap natural gas to lower their overall cost structures. In this case as well, some of the transition is permanent.

iv) At present, global natural-gas markets are not integrated. Prices are USD 0.75 Mcf in Saudi Arabia (subsidized by government), USD 3.9 Mcf in the US, around USD 12 Mcf in Europe and as high as USD 16 Mcf in Japan. Overtime market forces will narrow this gap. One such way of exploiting this arbitrage is exporting it to Asia. Export will eventually open up reducing the arbitrage and increasing natural gas prices.

v) Compressed natural gas (CNG) vehicles are very common in Asia. As of 2011, worldwide, there were 14.8 million vehicles that run on compressed natural gas (CNG), with approximately 5.7 million in the Asia-Pacific region followed by 4 million vehicles in Latin America. This number has been growing rapidly as CNG is a much cleaner fuel and produces much less pollution, is significantly cheaper than oil (Asian consumers are very sensitive to oil price) and has a lower maintenance costs than hydrocarbon-fuel-powered vehicles. CNG vehicles are encouraged by governments in Asia due to high pollution in these countries.

vi) Export of LNG is already on its way with the US sanctioning two LNG export terminals and another 12 waiting for approval. On 17 May 2013, the US Energy Department announced that it has conditionally authorized Freeport LNG Expansion, L.P. and FLNG Liquefaction, LLC (Freeport) to export domestically produced liquefied natural gas (LNG) to countries that do not have a Free Trade Agreement (FTA) with the United States from the Freeport LNG Terminal on Quintana Island, Texas. Freeport previously received approval to export LNG from its facility to FTA countries in February 2011. In May 2011, Cheniere Energy’s Sabine Pass, in Louisiana, was the first LNG terminal to get authorization to export LNG to non-FTA countries. Freeport’s and Cheniere’s combined capacity would amount to 5.2% of US production. As of 17 April 2013, 12 new LNG export terminals have been proposed in the US to Federal Energy Regulatory Commission (FERC) and there are currently 63 LNG export terminals planned or under construction worldwide.

7) Discount to peers: Apache has proved reserves of 2.9 billion barrels of oil equivalent (BOE) and is currently producing 779,000 BOE per day. This is in line with Anadarko (APC), its closest competitor. APC trades at an EV/EBITDA of 7.1x, price to tangible book of 2.1x and a forward P/E of of 16.1x as compared to APA’s multiples of 3.8x, 1.1x and 9.1x, respectively (see table below). APA’s stock price would have to increase approximately by 80% to trade at APC’s multiple.

| Comp Valuation | ||||||

| Ticker | Price | Market cap | P/tangible book | P/OCF | Forward P/E | EV/EBITDA |

| APA | 85.04 | 34,017 | 1.13 | 4.00 | 9.1 | 3.79 |

| APC | 86.71 | 43,360 | 2.08 | 5.24 | 16.1 | 7.14 |

| under value | 46% | 24% | 43% | 47% | ||

| DVN | 55.3 | 22,050 | 1.47 | 4.54 | 10.57 | 6.14 |

| under value | 23% | 12% | 14% | 38% | ||

8) Valuation: Despite taking heavy write-offs on various natural gas assets last year due to lower natural gas prices and increasing its debt to finance acquisitions, Apache’s trades at price to tangible book of just 1.1x (tangible book value per share of USD 77). This is historically low, even lower than 2008 levels. Also, on a price to EBITDA (P/EBITDA: 2.73x) and price to OCF (P/OCF: 3.9x) basis its trading close to or below 2008 levels.

9) Peak in capex: Capex (excluding acquisitions) has doubled from its 5 year average. It has risen from a 5 year average of USD 4.7bn to USD 9.5bn in FY12 and is still growing. As the company is investing significantly in capex to extract value from the recently acquired assets, capital expenditure will peak out in 1-2 years resulting in significant increases in production. Also, reduction in capex in the future will significantly increase free cash flow.

Risks:

i) Supply demand: As per International Energy Agency (IEA) report, for the period 2012-2018, world liquid capacity would grow by 8.4 million barrels per day, significantly faster than demand, which is projected to grow by 6.9 million barrels per day. This could depress liquid prices on the downside.

ii) Revenues heavily dependent on oil: Approximately 78% of APA’s total revenues come from oil.

iii) Selling oil at Brent price: Approximately 72% of APA’s crude oil production is priced relative to Brent crudes and sweet crude from the Gulf Coast, which continue to be priced at a significant premium to West Texas Intermediate (WTI)-based prices.

iv) Transportation: 71% of the oil consumption in the US is from transportation. In next 3-10 years fuel efficient hybrids, LNG, CNG and electric cars might be more common than we expect and the dynamics of oil industry could change significantly.

v) Environmental concerns: Fracking is relatively young, and probably not all of the environmental and geological consequences are fully understood. As time goes by, it is reasonable to expect more government regulations, which inevitably increases costs and could even put smaller producers out of the business.

vi) Egypt: Threats in Egypt include deterioration in the political, economic, and social conditions or changes in laws or regulations in the region, export restrictions, nationalization of APA assets and/or forced renegotiation or modification of existing contracts.

Hedge: For the above first 4 reasons, it is better to buy the stock with a hedge, downside protection to Brent oil. This makes sense especially now, as Brent is trading at 105, due to risks in Syria and Egypt.

Conclusion: In last 2 days stock has gone up by 3%. It is advisable to buy on dips. Market is neglecting APA’s diversified asset base and attractive long-term production growth in its asset rich shale plays and paying too much attention on Egypt, short term results and increased capex spending. Recent strategic acquisitions have huge potential still to be capitalized with room to improve margins and an enormous optionality on natural gas upside. The stock is significantly undervalued as compared to its peers and is trading below 2008 levels on valuation basis. Decline in oil price is a concern, by hedging the same one can bet on relative-value and a natural gas upside.

Company description: Apache Corporation, an independent energy company, explores for, develops, and produces natural gas, crude oil, and natural gas liquids. It holds interests in asset base of 12.3 million gross acres located in the United States; 7 million gross acres in Canada; 9.7 million gross acres in Western Desert, Egypt; 30 exploration permits, 17 production licenses, and 13 retention leases that cover a total area of 7.9 million gross acres in offshore Western Australia; 32 concessions, exploration permits, and other interests covering an area of 4.4 million gross acres located in 4 hydrocarbon basins in Argentina; and various properties located in the United Kingdom North Sea.

As of 31 December 2012, it had total estimated proved reserves of 1,441 million barrels of crude oil, condensate, and natural gas liquids; and 8.5 trillion cubic feet of natural gas. Combining both, Apache has proved reserves of 2.9 billion barrels of oil equivalent (BOE), and the company is currently producing about 779,000 BOE per day. However, including its Permian/Central resources that number goes up to 11.7 billion barrels of oil, four times higher than the current proved reserves. The company was founded in 1954 and is based in Houston, Texas.

Disclosure: Long APA, short Brent oil (via DTO)

Disclaimer: It is very important to read the disclaimer before making any investments based on the above article.

The Fake New Normal

Everything is great, keep the party going!

Europe: European problems are far from over. It is sinking in deeper recession with unemployment in 17 country Euro-zone at historically high levels of 12.1% and increasing. Retail sales dropped 0.1% in March from a 0.3% slide the previous month. Unemployment in Spain is now up 27.2% and mortgage delinquencies are continually rising. Portugal is moving toward a second bailout. Its government is considering to pay public workers in Treasury bills instead of cash. It also plans to slash 30,000 public sector jobs as a part of spending cuts. France’s business survey shows that it could enter recession (see chart below). Germany is faltering too with car sales in March down 12% y-o-y. While Slovenia’s creditworthiness is deteriorating as investors speculate a banking crisis in the region (see charts below). Banks in Slovenia are significantly undercapitalised with toxic loans now standing at 18% of GDP. All that said, Spain’s 10-year yield dropped to 3.8% for the first time since October 2010, yields on two-year Italian notes fell below 1% for the first time on record and 10 year Portugal bond yields dropped to 5.5.%, least since October 2010. This was after the ECB cut its main refinancing rate on 2 May and signaled it was open to a negative deposit rate. Conclusion: deteriorating fundamentals but significantly lower yields. Welcome to Matrix!

source: zerohedge

source: zerohedge

The US: It is not just Europe, the US macro economic data hasn’t been strong as well. 1Q13 GDP missed expectations and came in at 2.5%. Excluding inventory it would be at 1.6%, a very anemic growth. The total of ISM manufacturing and non-manufacturing index declined by 4.1% and 1.8%, sequentially, in March and April 2013. Construction spending tumbled 1.7% in April to a seven month low. Housing market index for the month of April was down. Thomson/Reuters Small Business Lending Index showed small businesses reduced their borrowing for a fourth month in a row and delinquencies on outstanding loan balances rose for the first time in more than three years. The ADP employment report indicated that the US economy added just 119,000 private-sector jobs in April, which was below consensus expectations of 155,000. People employed as a % of total civilian population (the real gauge of employment) in April was at 58.6%, pretty much same as in 2012 and just a little improvement from its historical low of 58.2% in July 2011. Most of the US macro economic data hasn’t met expectations but the market has ignored all of that and has only gone in one direction: north. Below is the chart showing the disconnect between economic data expectations (Bloomberg Economic Surprise Index) and S&P.

Source: zerohedge

Consumer Spending Fundamentals: Y-o-y growth in personal income has also been very anemic and below inflation, with y-t-d 2013 monthly average of 2.5%. Savings as a % of personal disposable income is currently at 2.7%, below 3% is a warning signal. With low income growth and already low savings rate, consumer spending, the engine of the US economy, doesn’t have a lot of room to run. Above all, q-o-q percentage change of personal income excluding current transfers is at recession levels (see chart 3 below). Also, the effect of tax increases (payroll and other taxes) comes at a lag and might be seen in the coming quarters. Lastly, people have forgotten about sequestration as if it never happened. Its impact has yet to begin.

Source: zerohedge

Source: zerohedge

Source: zerohedge

Sales growth and Margin expansion: Macro US data and Europe doesn’t matter, ultimately what matters are earnings and companies are beating expectations. Europe has been this way for a long time and market has understood to ignore it. Earnings is what market cares and companies have been beating expectations.

This is what the bulls argue. It is true, however companies have been beating only bottom-line by low-balling expectations. They have been missing on top-line. Sales growth is declining as the base is already high and the economy is growing at a slow pace. Sales growth is down from 9% levels in 2011 due to a very low base in 2010, to just 4% levels in 2012. So far in 1Q13, more than 50% of the S&P companies have reported earnings with more than 57% missing revenue estimates.

Also, corporate margins are at historic highs. Margins are mean-reverting and cannot keep going higher. S&P operating margins peaked at 9.5% (highest in last 13 year) in June 2012 and were at 8.0% in December 2012. The US corporates are the leanest historically and there is not much to squeeze to increase margins. Also, a lot of debt has been refinanced at super low rates reducing the interest cost which is one of the reasons for high margins. Conclusion: slowing sales growth and not enough left to squeeze to increase margins doesn’t sound like a good profitability recipe.

Source: zerohedge

Source: zerohedge

Current market P/E: market probably not that cheap: But markets are cheap, so all the above doesn’t matter as long we can buy good quality stocks for cheap.

Nothing is cheap in this market. March ending ttm earnings expectation for S&P are: as reported earnings: 88.06 (y-o-y inc of -0.5%), operating earnings: 98.78 (y-o-y inc of 0.7%). At these levels we have

Price to sales: 3 May 2013: 1.48; 31 Dec 2007: 1.43

PE (as reported earnings): 3 May 2013: 18.33; 31 Dec 2007: 17.36 (historical long term average is approximately 15.5x)

Price to book: 3 May 2013: 2.42; 31 Dec 2007: 2.77

All these ratios are above historical averages and equivalent to 2007 peak showing that the market is overvalued.

Flaw in S&P earnings estimate calculation: It doesn’t matter, future earnings expectations are high. Also, on a forward basis (FY13) market is cheap, trading at only 15x PE (reported earnings).

For FY13, analysts are expecting, as per S&P (as of 29 April 2013), a 14.2% increase in operating earnings to USD 110.5 and a 24.3% increase in as reported earnings to USD 107.6 (see graph below) (historical long-term earnings cagr is 4.8%). Considering the high sales base and end of productivity gains, I think, this is an optimistic view which makes S&P vulnerable. However, the main catch is how these forward earnings are calculated. This article on Seeking Alpha beautifully describes the mismatch between actual and expected earnings. The main difference is the pension expense. The crux being actual operating earnings are calculated by a different analyst which includes pension expense as a normal expenditure while estimates are calculated by another group of analysts which excludes pension expense while calculating operating earnings, as they consider pension expense an “unusual item”. This makes the expected earnings look inflated. So if the market is trading at high valuations (S&P already up 10.5% YTD, in just 4 months) based on expected earnings which are already inflated and the economic data is getting worse, probably it may not be a pretty scene. Conclusion: investing when it looks the easiest is at its hardest.

All the other asset classes and markets: While S&P keeps going in a straight line at 45 degrees, MSCI emerging market index is down, Europe is down, CRM commodity index is down, copper and steel has had a significant move down, personal income growth in the US is below inflation and banks are planning more job cuts. The market is conveniently ignoring all that. Apart from foreign risks (Europe’s debt crisis, Japan’s reflationary commitment, etc), the current overvalued market has a risk of rising interest rates, stopping of quantitative easing, reversing of historically high margins and probability of missing high earnings expectations.

source: zerohedge

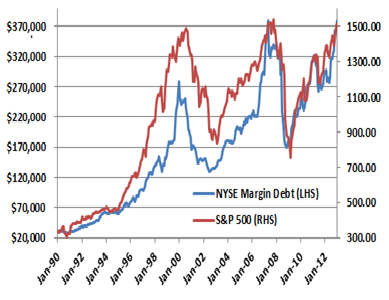

Who is buying?: Recent article by WSJ, Bond Funds Running Low on…Bonds, points out that the number of bond funds owning stocks is at its highest point in 18 years, showing that if bonds are in a bubble, equity is a place to go, even if that’s not their expertise. A sign that typically conservative investors are taking bigger risks to boost returns via dividend paying stocks. A clear consequence of money printing and significantly low interest rates, not benefiting masses at large instead making markets vulnerable. The other class of buyers is traders as no one wants to miss the rally. This has resulted in equity crowded trade. The below graph shows NYSE margin debt, which is at its all time high. Last two highs were in 2000 and 2007, when market peaked. If market falls, margin calls would be all over and the drop could be precipitous.

Japan: Who else is buying? The Japanese? The historically biggest Japanese quantitative easing is resulting in flight to safety from Japanese investors, who sense that their own bond market is on the verge of breaking down. This has managed to send French and Belgian bonds to record lows, the Spanish 2 Year to sub 2%, the German 6 month bill negative in the primary market, the US 10 year below 1.8% and 30 year sub 3%. Also, the yield-hungry-safety-looking Japanese are buying the US equities contributing to overvaluation and the fundamental disconnect. The immediate result is that the bond-equity disengage continues to diverge. Is this a new normal? If yes, it is not healthy and can’t go on for a long time.

FED support: Lets, for a minute, assumes how the economy would look if FED support is taken off. Excess liquidity goes away, interest rates rise and stocks fall. So the economy is still on FED crutches and an overvaluation in such a scenario only shows irrational exuberance. Assuming that the consequence of money printing is just positive is naïve. Also, assuming that a slow withdrawal of money printing would be smooth and easy is an irrational thought. No one has been able to do it, the Germans, the Japanese, the Argentinians etc have all failed. We have seen countries stuck in the liquidity trap and unable to exit but never there is an instance when a country exited smoothly without any pain. The question now is that if 5 years of massive QEs cannot revive the economy, what can? Also, if the market falls, people will start doubting the effectiveness of QE.

The incomplete cycle: Lastly market operates in cycles. A common saying is that get your companies right and don’t worry about Mr. Market. He will have mood swings but eventually you will be rewarded for picking up the right companies. They forgot to mention the price. Price is everything. Equity market can be dead for more than a decade and make you extremely rich in another decade. The concept of market cycles has been proved historically era after era. Below table shows 16 year market cycles from 1886 until present. The current cycle looks incomplete with a positive return instead of a negative cagr.

Most people fail to recognize that absence of immediate crisis doesn’t mean that we won’t eventually face one and that the consequence of money printing isn’t just positive. In a global central bank money printing environment where economic fundamentals don’t matter, VIX at a complacently low level of below 13, major continents in recession and earnings based on overly optimistic future expectations, I guess one should think twice before investing. What we know for certain is that during the most recent market cycle, the repeated hope that stocks could detach from the economic data proved to be unfounded in nearly every instance: 2010s fall in May and June, 2011s fall in August and September and 2012s fall in May and June. When debt to central bankers or economists doesn’t matter: debt growing from USD 6 trillion to USD 16 trillion in past 12 years, it is time to take a step back and think.

Most people fail to recognize that absence of immediate crisis doesn’t mean that we won’t eventually face one and that the consequence of money printing isn’t just positive. In a global central bank money printing environment where economic fundamentals don’t matter, VIX at a complacently low level of below 13, major continents in recession and earnings based on overly optimistic future expectations, I guess one should think twice before investing. What we know for certain is that during the most recent market cycle, the repeated hope that stocks could detach from the economic data proved to be unfounded in nearly every instance: 2010s fall in May and June, 2011s fall in August and September and 2012s fall in May and June. When debt to central bankers or economists doesn’t matter: debt growing from USD 6 trillion to USD 16 trillion in past 12 years, it is time to take a step back and think.

Disclosure: long S&P put spreads

Disclaimer: It is very important to read the disclaimer before making any investments based on the above article.

End of a superpower: Japan’s next decade

Long: CDS on Japan or Out-of-the-money put options (or put spreads) on Japanese interest rate swaps

Trading at: 1 year CDS: 55bps 5 year CDS: 126bps 10 year CDS: 164bps

Upside: Best case: 509% to 966% (cagr of 44% to 81%) Base case: 335% to 611% (cagr of 23% to 39%) Worst case: 238% to 433% (cagr of 15% to 23%)

Time period: 5 years to 7 years

Understanding Japan:

In 2011, Japan was the third largest economy in the world after the United States and China. Japanese economy grew at an average rate of 7.5% in 1960’s and 1970’s (aka Japanese post-war economic miracle) and 3.2% in 1980’s and early 1990’s before the burst of its real estate bubble. Until 1990’s, before the Japanese property and stock market crash, Japanese households saved and businesses borrowed. When there were not enough borrowers for the available savings the economy would weaken and Bank of Japan (BOJ) would lower the interest rates. When there were too many borrowers, the economy would overheat and interest rates were raised. The end result in either case was that savings were borrowed and spent, which resulted in growth. When the Japanese stock and real estate market collapsed in 1990’s, asset prices plunged while debt was still on the corporate balance sheets. The fear resulted in deleveraging by the corporate world. This led to a significant decrease in borrowing and hence slow growth regardless how far BOJ lowered interest rates, creating a surplus of private savings. To reverse the situation and to stimulate spending, BOJ borrowed those surplus private savings and started spending in the form of stimulus. It’s been borrowing and spending since then, which has inflated BOJ’s debt to very high levels and has resulted in 2 lost decades of economic growth.

What fuels Japanese Government Bonds (JGB’s):

Large savings by the household sector and corporate Japan have fueled the JGB market. As of 2010, financial assets held by household sector (1,488tr Yen) and corporate Japan (454tr Yen) were 1,942tr Yen, while liabilities of the same were (361tr and 854tr Yen, respectively) 1,215tr Yen.4 These savings, directly or indirectly, are invested in the JGB market via Japanese banks. This has been the reason that Japan has been able to sustain huge levels of debt by borrowing 95% internally.

Fuel from corporate Japan: The below graph (chart 1) shows that cash and deposits held by all industries in Japan has remained pretty much stable but the investment in securities by corporate Japan has increased consistently and notably in last few years (until recently), fuelling the JGB market. Corporate Japan has been increasing its annual investment in securities by an average of 10.2tr Yen in last 5 years and 8.8tr Yen in last 10 years.

Chart 1

Household savings: Japanese household still (as of 2010) have a savings rate of approximately 35%, which is approximately 73tr Yen on a yearly basis. A lot of this money flows into Japanese banks in the form of savings account or deposits which help fuel JGB’s.

Japanese banks having fewer options: Over the past decade, a gradual increase in deposits and a decline in corporate loans (chart 1) have provided additional space for investments in JGB’s. Since 2000, household deposits have increased while demand for bank loans (short and long term, chart 1) by corporate have declined. These two factors have led to a decline in the loan-deposit ratio from 95% in 2000 to 70% in 2011 for Japanese banks. More deposits in banks and fewer options to invest have resulted in significant increase in their JGB holdings.4

Intervention by Bank of Japan (BOJ): BOJ has increased purchases of JGB’s (currently at 21.6tr Yen per year on a gross basis) since the beginning of the global financial crisis. It has been acquiring government securities through the new asset purchase program, which has resulted in stable yields. 4

That being said, Japan issued 40tr Yen in 2011 and 44tr Yen in 2010. Adding corporate Japan investments in securities and Japanese household savings gives us 83tr Yen (73tr Yen + 10tr Yen, as mentioned above) on a yearly basis of which some flows into JGB’s. Assuming that BOJ keeps intervening in the JGB market and buying JGB’s through the asset purchase program, (which I don’t think is possible for a very long period of time) still approximately 25%, 21tr Yen (25% of 83 = 21), of the corporate and household savings should be directed to JGB market for it to sustain itself. Household savings (approximately 90% of the total 83tr Yen) are expected to decrease due to aging population while the issuances of JGB’s are expected to increase due to increased expenditure related to aging population and the debt service cost. I have researched thoroughly and have done an in-depth analysis to understand if the next decade could be the end of a once superpower reaching the Keynesian end-point.

Fundamental problems of Japan:

Quantitative issues:

Fiscal deficit:

Japan is spending more than twice of what its earning (chart 2). As of 2011, its yearly expenditures were 212% of its revenues. The below graph shows that the fiscal deficit is only getting worse due to declining revenues and increasing expenditures, both of which are a factor of Japan’s aging population and negative population growth.

Chart 2

Table 1

Social security and debt service costs: Japan is financing these fiscal deficits by issuing Japanese Government Bonds (JGB’s). It has been trying to cut its spending but is unable to curb its social security and debt service expenditures, which are a major component (28% and 20%, respectively) of its total expenditures (see table 2. I have excluded year 2011 in compounded annual growth rate calculation due to earthquake and tsunami in Japan, which is a one-time event and has resulted in increased government expenditures for 2011). These expenses will only increase and get worse as Japan’s 65+ age group has grown exponentially and is highest as a percentage of its population in the world. In addition, in 2007 Japan’s population growth rate turned negative. In next 5 years population of age group 65 years and above will increase from approximately 23% of its total population in 2010 to an estimated 27.5% by 2015. As modeled, this can increase the annual social security expenditures by an estimated 70% by 2018. Such high social security costs along with declining revenues would make it difficult for Japan to handle its fiscal deficit.

Table 2

Debt levels and interest rate:

As previously mentioned, when the Japanese stock and real estate market collapsed in 1990’s, asset prices plunged while debt was still on corporate balance sheets. The fear resulted in deleveraging by corporate world. This resulted in significant decrease in borrowing regardless how far BOJ lowered interest rates, creating a surplus of private savings. To reverse the situation and to stimulate spending, BOJ borrowed those surplus private savings and started spending in the form of stimulus. It’s been borrowing and spending since then, which has inflated BOJ’s debt to very high levels. Japan’s debt as a percentage of revenues has increased from 3.4x in 1990 to 19x as of 2011, a very high leverage (chart 3). This will only get worse in the future as the revenues are declining while the expenses are going up, adding to the overall debt.

Chart 3

Japan has been able to sustain this by borrowing internally from its people and corporations. Domestic buyers hold about 95% of the nation’s debt, according to the Japanese Ministry of Finance. Even though the country’s debt has increased significantly after the burst of the 1990 bubble, interest rate on its debt has gone down drastically. Interest rate on JGB’s has reduced from 5.5% in 1990 to 1% as of 2011 because of low growth (0% to 1%) and zero interest rate policy (chart 4). With such low interest rates, interest payments on JGB’s are 20% of its revenues. Besides, as mentioned above its debt to revenue was at 19x as of 2011. As modeled, it can reach to approximately 28x by 2018. At such high levels a small change in interest rate could increase the interest payments considerably. In addition, given the high correlation between yields on JGB’s and other sovereign debts, a sudden rise in global risk premia could have a spillover effect on the JGB market. In 2011, with a leverage of 19x, implied interest rate on JGB’s increased by 20 bps to 1.1% which resulted in an increase in interest expense by 27%. Interest expense increased to 20% of revenues in 2011 from 14% in 2010 with just a 20 bps move in rates (as of Sep 2011 interest expense was 10% of revenues for the US with an implied interest rate of 2.9% on its total debt). If the interest rate on JGB was to rise to 2%, interest payments could reach as much as 53% of the revenues and debt service 75% of revenues by 2018, virtually making Japan broke. Most of its revenues would just go to service its debt and for all its other expenses such as social security, education, defense, public works, energy, local allocation, etc (which presently account for 80% of its total expenditures and are growing) it would have to issue more debt. The question is would the interest rate on JGB increase?

Chart 4